If you’re like most other Americans, you likely never learned much about finances growing up. Only 22.7% of high school students in the U.S. had guaranteed access to Personal Finance courses as of 2022. Some of us made a little cash with side jobs, but after high school we were expected to step into heavy debt without learning much about it.

Around 80% of Americans have some form of debt, and if you grew up in a home where money was tight or considered a stressful topic, you probably didn’t learn much about financial literacy at home.

Most of what I have learned has come from years of talking with others, but for simplicity’s sake let’s nail down a few of the main topics when it comes to finances.

Debt

Whether it’s loans for school or credit card debt, target the one with the highest interest rate first as that will cost you the most over time. If you have to get an unsubsidized loan for school, you are responsible for paying interest on that from day one, unlike a subsidized loan where interest doesn’t accrue until leaving school (and after the 6-month grace period). If you need a short break in payments and decide to do student loan deferment, the unsubsidized loans will continue to accrue interest, so you may want to continue paying it during the deferment period.

Using a credit card can help you with cash-back benefits and with building a credit score, which you’ll need for renting an apartment, good rates for car and homeowner’s insurance, and lower interest rates for personal loans. Depending on your state, employers may also check your credit score to decide who to give a job or promotion to. But if you can’t pay off your credit card bill every month, you should stop using it. The very high interest rates are not worth the risk.

Saving

Once you’ve paid off those high-interest debts and have your financial feet on the ground (woohoo!), let’s talk about saving. The general consensus is to save enough money to cover your basic living costs for 3-6 months. I suggest putting it into a high-yield savings account so that you’ll continue to make some interest on it every month. I use Capital One 360 to get a passive income around 4.5% a month, but there are many so do some research. Transfers between your high yield savings account & your bank should only take a few days, so the money is fairly liquid unlike with investing.

Retirement

Now that you’ve got your financial cushion in case of emergencies set, let’s talk about retirement.

According to the Pension Rights Center, only 56% of full and part time civilian workers participated in a retirement plan at work in 2023. Since about half of all Americans do not have a retirement plan at work, we need to make a plan for ourselves.

Personally, I go with a Vanguard Roth IRA Target Retirement Fund, though you can research other Target Date Funds with other providers. The goal of the fund is it changes the investments from riskier with higher gains when you’re younger to conservative and safer investments as you age towards retirement. There is an annual limit on investment (currently 7K) which I’d recommend making your target to max out on, but if you can only afford $50 a month at first that’s fine too as long as you develop that healthy habit.

Investing

I’m only going to discuss traditional investing and not day trading. Investments are for the mid- to long-term, and as I didn’t start learning about it until 2020, so I was investing into the red for a long time until I started turning a profit. When thinking long-term, the market ups and downs don’t matter as much, since in 10 year’s time there will be overall growth. The safest bet is to invest a certain amount every month (e.g. $270), though you could invest less when it’s a bull market (rising) and more when it’s a bear market (falling).

There are many stock trading apps and I haven’t done much research into them, but I personally like Robinhood. While I have tinkered in utilities and dividend investments, most of my investments are in ETFs (“exchange-traded funds”). They are less risky than individual stocks because they have a bundle of assets which means there’s diversity. You may want 5-10 ETFs to invest into. I’m still not a master at all of this, but the ETFs I like are ESGV (sustainable investing), VTI (total stockmarket ETF), VOO (S&P 500 ETF), VIG (dividend ETF), VUG (Vanguard Growth ETF), BND (bond ETF).

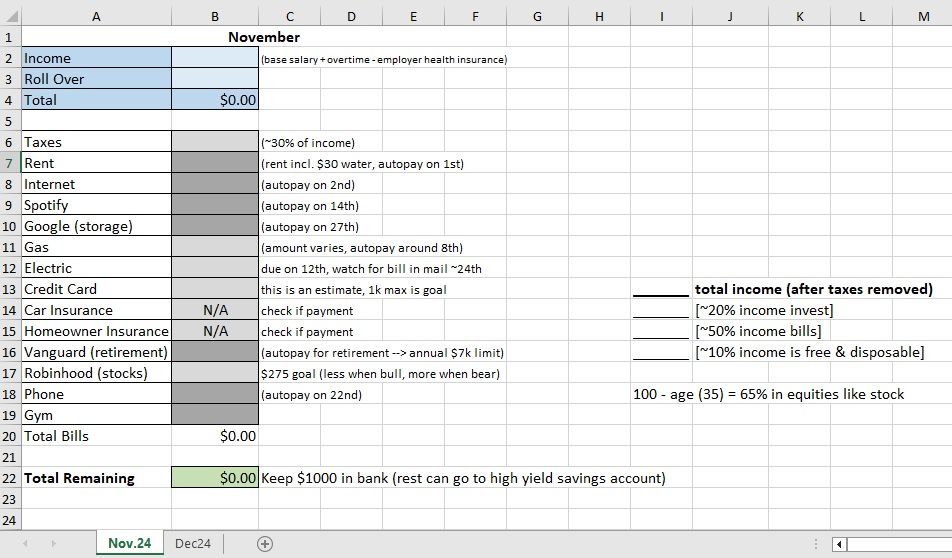

Budgeting

I’m fairly organized, so I’m not sure how I would do things if I didn’t have my monthly budget on an excel file. You may have your own system, but feel free to pull ideas from this if it seems helpful.

(Dark grey highlights automatically pay a decided amount, but the light grey ones indicate where I need to follow up monthly.)